QuantWeave

Modelling probability of an event using poisson process

We look at how to model the probabability of an event by using jumps in a poisson process.

Static replication using Breeden-Litzenberger

We use Breeden-Litzenberger to compute option prices numerically and replicate payoffs statically.

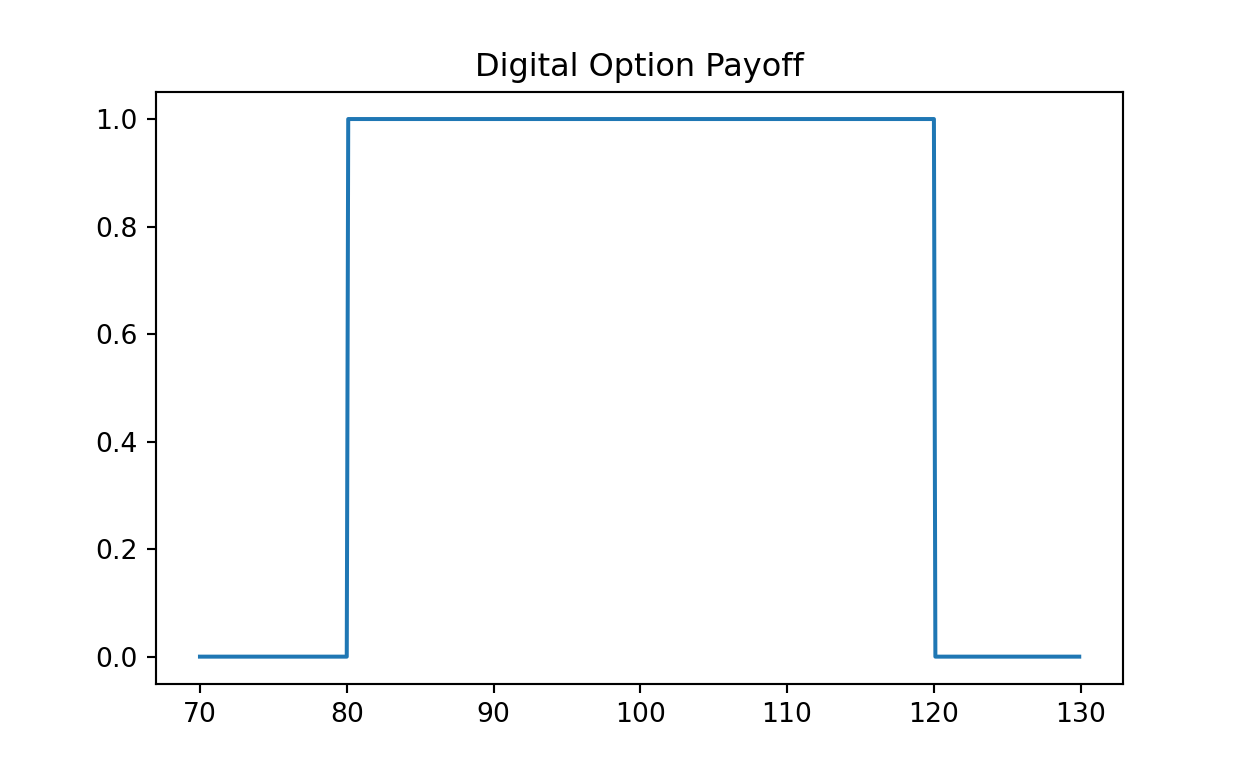

Replicating payoff of digital option

We explore payoff replication of exotic options using a portfolio on vanilla options. We investigate how well the replication is and what factors affect the payoff.

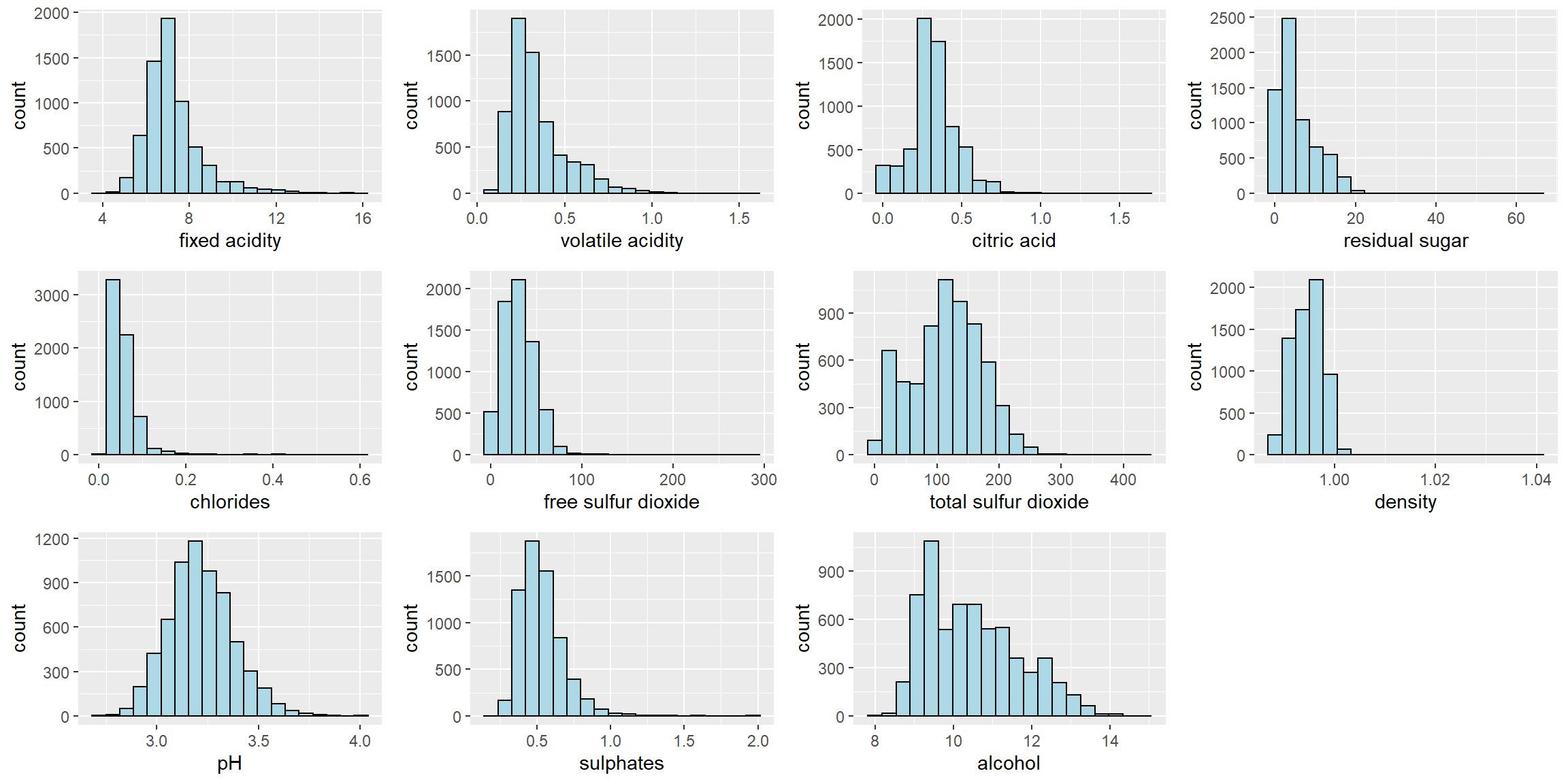

Using R to visualize data

We use popular R packages to visualize static data through histograms.

Motivations behind QuantWeave

A deep-dive into quantitative methods and data science to solve real-world problems. I started this blog as a medium to bridge quasi-methods to the world of finance.